PBoC exerts greater control over overnight lending rates

China’s central bank (PBoC) is strengthening its influence over overnight lending rates, paving the way to a shakeup in how it guides the economy.

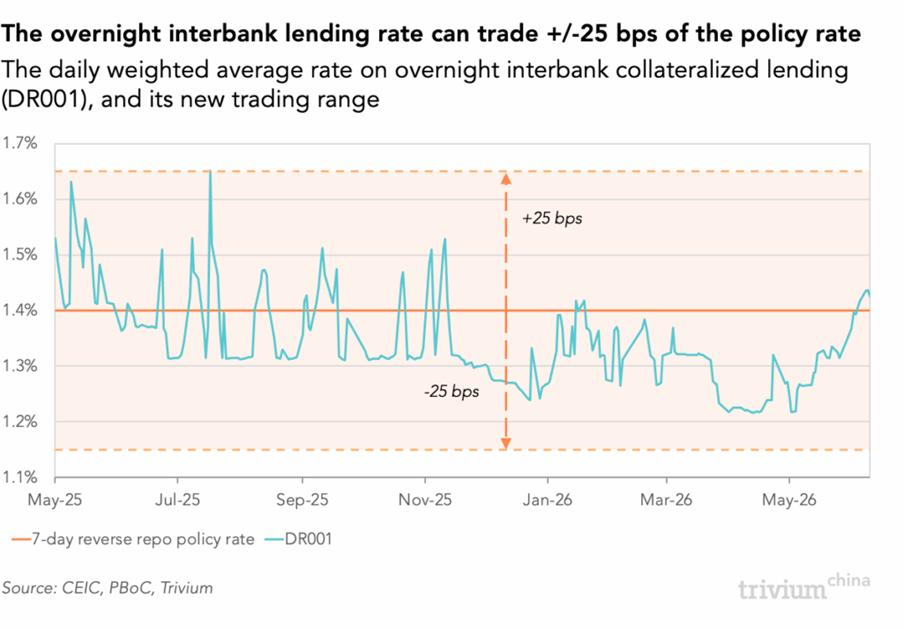

The details: On June 17, the PBoC said the rate on overnight interbank collateralized lending (known as DR001) will be permitted to trade 25 basis points above or below seven-day reverse repos the PBoC sells during open market operations (OMO) – which is the PBoC’s main policy rate.

- The previous range was 35 bps either side of the reverse repo rate.

Meanwhile, in comments made the same day at the Lujiazui Financial Forum, PBoC Governor Pan Gongsheng said the central bank will introduce more varieties of overnight reverse repos into OMO.

Some context: For years, the seven-day interbank collateralized lending rate (DR007) has been the benchmark for pricing short-term credit. The PBoC has guided the DR007 using its seven-day policy rate.

- While seven-day lending benchmarks aren’t unheard of, the central banks of most major economies – including the US Fed – use overnight rates to manage the economy.

The PBoC has engaged in buying and selling overnight reverse repos since July 2024, for a 20-minute window each afternoon.

- However, whereas the PBoC uses other maturities of reverse repo to manage liquidity, it uses overnight reverse repos as a way to ensure the overnight rates stays within the trading range.

- It sells overnight repos at 20 bps below its seven-day policy rate and buys them at 50 bps above.

Get smart: There’s been widespread speculation that the PBoC might follow in the Fed’s footsteps.

- That would require ditching the seven-day reverse repo as its policy rate and replacing it with an overnight rate.

- We’re not there yet, but the PBoC just took a step closer.