China’s strong Q1 GDP print masks underlying weaknesses

China's economy grew strongly in Q1 2026 – but momentum is starting to wane.

Per data released by the stats bureau (NBS) on April 16:

- GDP grew 5.0% y/y in Q1, up from 4.5% in Q4 2025.

- On a quarter-on-quarter basis, the economy expanded 1.3%, up from 1.2% in the previous quarter.

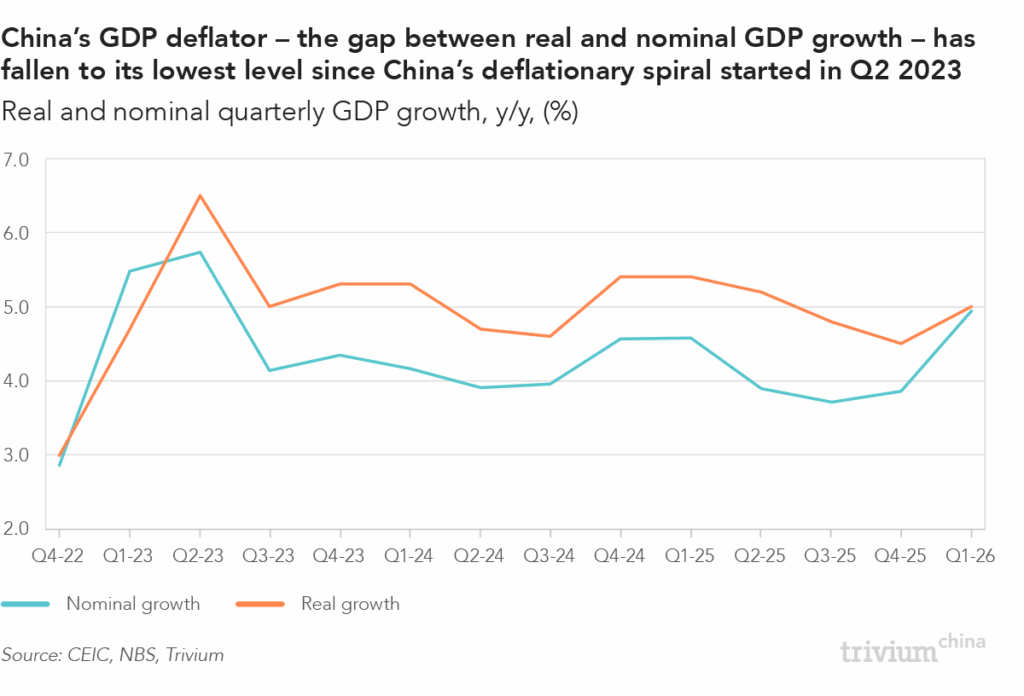

Deflationary pressures are easing: Nominal GDP growth – which incorporates price effects – came in at 4.9% y/y.

- While real growth has now exceeded nominal growth for twelve consecutive quarters, the gap between the two has narrowed to its smallest since China's deflationary spiral began in Q2 2023.

The headline GDP print is solid, but March's monthly activity data paints a less rosy picture:

- Industrial value-added (IVA) grew 5.7% y/y – a decent clip, but down from 6.3% in January-February.

- Private sector IVA – which gives a purer read on market-driven activity – grew just 4.0%.

- Retail sales of consumer goods grew 1.7% y/y, slowing from 2.8% in January-February.

Get smart: Q1 growth was strong, partly because the broader macroeconomic impact of the Iran war only began to bite in March.

- The deterioration in monthly activity data could be an early signal of what's coming in Q2.

Get smarter: The narrowing gap between real and nominal growth suggests China is edging out of its deflationary spiral – but the Iran war complicates that reading.

- Cost-push inflation is not the same as a genuine demand-led reflation, and as we have argued elsewhere, it compresses margins and squeezes household purchasing power rather than expanding it.

sources

NBS: 一季度国民经济实现良好开局